“Cost sharing” refers to people paying money out of their own pocket to receive healthcare services. There are lots of forms of cost sharing—the most common ones are deductibles, copays, and coinsurance.

When healthcare reformers talk about cost sharing, they are often arguing that we should increase cost sharing so that people will stop overutilizing health services (especially low value ones). They call it getting consumers to have some “skin in the game.” The Rand Health Insurance Experiment found that this works, although people decrease their utilization of high-value services as well.

But this isn’t the thing we need cost sharing to do for us. What we need it to do is get people to start considering prices when they choose where to get care.

If people don’t care what the price of a procedure is, there’s no reason they would go out of their way to find one that is less expensive (while being of at least equivalent quality). In fact, they probably wouldn’t bother checking prices at all.

But when they are forced to pay at least some part of the price, they will start asking questions to find out the price of their options. Not everyone will, of course. But some will start doing that, especially when they discover that they could potentially pay thousands of dollars less for no worse quality.

Trying to find prices is a frustrating endeavor in our healthcare system because prices are still hard to come by. And often even the quoted price is an estimation, or it doesn’t include the same bundle of services as another provider’s quoted price.

But if people can successfully find prices and choose ones that are lower priced, do you know what happens? Providers start to see that their prices actually do impact how many patients choose to receive care from them. And then the market actually starts to function because competition (at least over prices) has begun.

To summarize, we don’t need cost sharing for the sake of skin in the game; we need it so patients can be put to work searching for the best deals (trying to save their hard-earned money) because this searching effort is the main prerequisite for competition.

By the way, I am not saying people need to pay the full price of every service. The key is that they pay at least some amount of the price differential between options. So if one provider quotes $4,000 and another quotes $5,000, all we need is for them to pay is a little more if they choose the $5,000 one. This could be through reference pricing, where they pay the full $1,000 difference. Or through other methods that only have them pay part of that $1,000, such as high coinsurance or tiered networks. There are many ways to achieve this.

This is one of those topics that comes up in healthcare reform discussions regularly, but we don’t often take the time to explain it. It’s not currently a trending topic, but it’s a perennial one, so it will come up again sooner or later.

Let’s start with an assumption: All people want health insurance.

But people’s willingness to pay for health insurance varies greatly. If it’s free, few would refuse. If it costs $200 per month, many more would refuse. If it costs $2,000 per month, most would refuse.

What determines whether someone thinks the premium is worth it?

A few things. The two biggest factors are (1) how much healthcare that person expects to need that year and (2) how much money they have. If a person expects to be hospitalized multiple times that year, a $2,000/month premium is probably going to be a lot less (even with the deductible and copays) than going without insurance. If a person is fairly wealthy and has the foresight to recognize that unpredictable healthcare expenses could be financially catastrophic, they would probably also be willing to pay the $2,000 deductible. But healthy people and poor people (and especially poor healthy people) are much less willing to spend much on premiums.

Ok, that was most of the background information, and here’s one more thing. If an insurance company is allowed to charge whatever they want for a premium, you know what they would do? They would collect a bunch of data on every insurance applicant and use some smart actuaries to calculate each applicant’s average expected annual healthcare spending, and then they would use that number (plus a percentage) for the person’s premium that year.

As you would expect, this would work fine for the young and healthy who will have low premiums. But for most others, it can be pretty expensive to the point that many would rather choose to forego insurance.

Now we can talk about how to cause a death spiral.

To solve that problem of premiums being too expensive for the people who probably need insurance the most and ending up uninsured, the government can make a simple policy that requires insurance companies to charge everyone the same premium. (For simplicity, I’m saying they will only have a single premium, although in reality they usually say something like, “You can only charge the sickest person 3x what you charge the healthiest person, and you can only use these few variables to decide who is sick and who is healthy.”)

What happens? The sick people get a great deal, and the healthy people end up subsidizing the sick people’s premiums.

This enables the sick people to get insurance, although now that the healthy people’s premiums are so expensive relative to what they’re getting out of it (many of them probably don’t even end up using their insurance most years), they say, “Forget that. Buying insurance isn’t worth it anymore.” And they drop out of the insurance pool in favor of going uninsured.

What happens then? All the healthiest people are no longer in the insurance pool, so the average expected healthcare spending per person will be much higher the next year. Therefore, the insurer is forced to raise premiums accordingly.

And, predictably, when those new higher premiums come out, again the healthiest in the insurance pool will say, “Last year it was just barely worth it for me, but this year with this crazy increased premium, it’s not worth it.” And they drop out of the insurance pool. This is about the time when the insurance companies get labeled as greedy, too.

The next year, premiums rise again, and more people forego insurance.

Do you see the pattern? That’s a death spiral. And, again, it’s caused by requiring insurance companies to restrict the degree to which they can charge different people different premiums.

There is a way to prevent this, though. If, at the same time as restricting premiums, the government also creates some sort of incentive for healthy people to stay in the insurance pool, it can prevent them from leaving.

That’s what the individual mandate was for. It was the government saying, “Hey, we need you healthy people to be in the insurance pool subsidizing the sicker people’s premiums, so we’re going to persuade you to do that by making you pay a fee (tax) if you don’t buy health insurance.”

It didn’t work very well. Many people didn’t know about it, and those who did figured they’d rather pay a relatively small tax than a relatively large insurance premium. That’s why premiums in the private market rose so quickly after the Affordable Care Act was passed. Not enough healthy people joined the insurance pool, and more dropped out each year. It wasn’t exactly a precipitous death spiral, but that is the direction it was trending.

Last week, I posted the salient direct quotes from Joe Biden’s official campaign website talking about how he will try to fix the healthcare system. This week, I’d like to go through the main big-picture parts of his plan and explain their context and rationale. Then, next week, I’ll conclude this short series by making some predictions about how effective his plan will be and recommending some important changes.

First, possibly due to political feasibility, he isn’t pushing for Medicare for All. He wants to keep the Affordable Care Act (the ACA, or “Obamacare”) and fix the parts of it that aren’t working so well.

So let’s take a look at that.

There are many parts to the ACA, but its main thrust was to increase insurance coverage. Here are some 2019 data to show what kind of numbers we’ll be working with in this discussion:

People over age 65 are on Medicare (60,000,000 people), so that’s straightforward.

But for the rest–the under-age-65 people–they fall into one of four insurance groups . . .

Employer-sponsored insurance (160,000,000 people) if they’re lucky enough to work for an employer that provides benefits

Medicaid (70,000,000 people) if they’re poor enough to qualify

Private insurance from the “private market” (10,000,000 people) if they make too much to qualify for Medicaid and don’t have an employer that provides benefits

Uninsured (30,000,000 people) if they don’t get insurance from their employer, they don’t qualify for Medicaid, and they don’t want to fork out the dough for insurance from the private market

Now, how did the ACA work to decrease the number of uninsured people? There were many ways, but here are the two biggest ways:

First, it allowed states to liberalize their eligibility criteria for Medicaid, and it offered federal funds to pay for most of the costs associated with all those new Medicaid enrollees. That accounts for about 12,000,000 of that 70,000,000 number listed above, some of which were previously uninsured, and others of which were previously on private insurance.

Second, it created a tax (also called a “health insurance mandate”) for anyone who didn’t have health insurance. This was to push the uninsured who didn’t qualify for Medicaid to buy insurance. And because everyone was going to be required to buy insurance, they had to make sure it would be affordable for everyone, so they promised to help cover the cost of insurance premiums for anyone under 400% of the poverty level. And to prevent insurance companies from taking advantage of the government’s willingness to help pay for people’s insurance premiums, they made a rule that insurers have to charge everyone the same premium (although that price can be adjusted up or down to a limited extent depending on two factors only: age and smoking status).

So, an easy way to describe the ACA’s second way it was trying to increase insurance coverage is by saying it was attempting to shift uninsured people into that private market. The ACA even created a nice website (healthcare.gov) to make it extra easy for people to shop for insurance plans on the private market by listing them all there side by side in a standardized fashion, and the website went so far as to pull in people’s tax information to calculate their premium subsidy right up front as well.

Unfortunately, most of the uninsured who didn’t newly qualify for Medicaid still didn’t buy insurance, not only because the tax/mandate was initially weak, but because it was subsequently eliminated. But the sick people are still buying insurance in the private market because it’s worth it for them since their premium is the same as everyone else with their same age and smoking status. This has left that private market’s risk pool with horribly high average risk and, therefore, horribly high premiums, especially for anyone who earns more than 400% of the poverty level and therefore doesn’t qualify for any premium subsidies. And that’s why there are still 30,000,000 people who are uninsured.

The natural solution to this would be to restore the mandate and to get rid of the 400% poverty level limit and just decide to subsidize the premiums for anyone whose premium will amount to, say, more than 8.5% of their annual income. This would shift many healthy people back into the private market and bring premiums down a whole lot by lowering the average risk, which would then pull even more people from the uninsured group into the private insurance group.

And that’s exactly what Joe Biden plans to do. Except for the reinstating the mandate part, which would probably not be popular nor even possible. I guess he hopes that if his subsidies are generous enough, he will get more healthy people into the market even without a mandate.

He is making the subsidies extra generous. Not only can anyone qualify now (as long as their premium is going to be more than 8.5% of their annual income), but also the benchmark plan these subsidies are based on are gold level plans rather than silver (meaning out-of-pocket costs, especially deductibles, will be a lot lower). So we will see how many of those 30,000,000 people will be enticed into buying health insurance.

But he’s gone further than that. I think he feels that insurance companies don’t truly competitively price their plans because he’s also going to create a new publicly run insurance company that will offer its own plan (known as a “public option”) in the private market alongside all the other private insurers’ plans on healthcare.gov. If the public option ends up being way cheaper than all the other private insurance companies’ plans, everyone will choose to get on that public option, and it will force private insurers to start pricing their plans more competitively. This should also help to lower prices in the private market, which will price even more uninsured people into the market.

There are lots of other details to his plan (you can read them in last week’s post), but the parts discussed here are what I believe to be the biggest core pieces. Everything else is somewhat peripheral.

I have lots of thoughts about how this plan into fits into/contributes to/detracts from the overall changes that need to be made in our healthcare system, so look forward to those next week.

This is the final installment of the Building a Healthcare System from Scratch series, and it begins with the same caveat as Part 7—to understand the rationale behind the ideas presented, you need to read and understand all the prior parts of the series, beginning at Part 1.

Now that I have explained the Healthcare Incentives Framework (Parts 1 through 6) and described what various types of systems would look like that have implemented the principles of it (Part 7), we are ready to look at something more complex: rather than building an optimal system from scratch, how can this framework be applied to an existing system that needs fixing? The American healthcare system will be a perfect case study for this.

Where it sits right now, the American healthcare system seems to land somewhere in between the libertarian-type system and the single-payer system described in Part 7, except that it fails to implement the majority of the principles of the framework. It is also overly complex, which contributes greatly to its impressive administrative expenses. So what could a much-simplified American healthcare system look like that also maximally implements the principles of this framework? With consideration for and much guessing about Americans’ preferences regarding healthcare, here is an imagined description . . .

The United States eventually chose to strengthen its individual mandate. The government now mandates all people, without exception, to have a healthcare insurance plan that covers all services included on its list of “essential health benefits.” For those who forego insurance coverage, they pay a tax penalty that ends up being nearly the same as the premiums they would have paid. If uninsured individuals receive care that they cannot afford, they usually end up having to either go on long-term repayment plans or declare bankruptcy because there is no bailout available for them.

The website healthcare.gov has become the ultimate source for healthcare insurance shopping. All qualified insurance plans (i.e., plans that cover all the essential health benefits) are listed there, along with their coverage level (according to the metal tiers), prices, and a short description that highlights any other benefits the plan offers that may help prevent healthcare expenditures.

Premium subsidies are available to all whose premiums will exceed a certain percentage of their income, and the subsidy amount is pegged to the second-cheapest qualified insurance plan available to them. The subsidies are automatically applied at the time people are choosing a plan on healthcare.gov. Because this system worked so well and was basically duplicative of Medicare and Medicaid, both programs were slowly phased out, which decreased insurance churn and increased time horizons. However, a vestige of Medicaid remains in that, depending on an individual’s annual income, there are also limits on how much they can be required to pay out of pocket for care.

The government also did away with the employer mandate and somehow found the political willpower to repeal all tax breaks for healthcare expenditures, which eventually led to employers getting out of the business of providing healthcare insurance for their employees and just giving that money to employees directly as regular pay.

Altogether, these changes mean that all Americans shop for their healthcare insurance on healthcare.gov. For anyone who is unable to do this themselves, there is a phone number to call to connect with someone who can assist them in selecting the plan that seems best for them.

A few changes were also made to encourage more insurance options. First, many regulations were eliminated, including the medical loss ratio requirement and state insurance department approvals of rates. These became unnecessary after people began to be able to compare the value of different insurance plans and choose based on that because overpriced or low-value plans (either from too much overhead or too high of rates in general) lost market share and profit. State-specific insurance regulations were standardized so that insurers can easily expand to new markets. And a law was passed requiring transparency of all price agreements between providers and insurers, which made the process of forming contracts with providers in a new region easier. These policies led to almost all markets having multiple options for each coverage tier.

In this way, the United States achieved universal access to affordable healthcare insurance relying on the private market while preserving the ability and incentive for all people to select the highest-value insurance plan for them. As a result, insurance plans aggressively innovate to find ways to prevent care episodes so that they can offer lower premiums and attract higher market share. Insurers also found that implementing differential cost-sharing requirements led people to start choosing lower-priced providers, which also enabled the insurer to lower premiums further. Finding provider prices has become easier ever since the price transparency law was passed.

The government has had to help overcome the problems caused by a multi-payer system by enforcing some standardization, including uniform insurance forms/processes, standardized bundles of care that all insurers in a region either agree or disagree to implement together, and standardized quality metrics that providers are required to report. These quality metrics are not used for bonuses, so they have been changed to be more focused on what patients need to know to choose between providers for specific services.

These quality metrics are now reported on an additional section on healthcare.gov that lists all providers, their quality metrics, and their prices (seen as your expected out-of-pocket cost if you log in) in an easy-to-compare format. Due to patients’ differential cost sharing requirements for most services, as well as broad common knowledge of the existence and utility of this website, most patients have begun to refer to it before choosing providers. This part of healthcare.gov has even been developed into a highly rated smartphone app.

In response to these changes, providers found that their value relative to competitors largely determined their market share and profitability, which unleashed an unsurpassed degree of value-improving innovation. The cost of care in the United States was previously so high that the majority of those initial innovations led to much cheaper care, which led to much lower insurance premiums and eased the premium subsidy burden on the federal government. Thanks to these changes, the federal deficit has begun to sustainably diminish quicker than any budgetary forecasting model could have predicted, which has also helped stabilize the American economy.

There are still barriers to people being able to identify and choose the highest-value insurers and providers. There are many important aspects of quality that are unmeasurable. Many people do not have the health literacy required to figure out which insurance plan or provider would be best for their situation and preferences, despite the ease of comparison enabled by healthcare.gov. There are medical emergencies that do not allow shopping (although the number of these has turned out to be much less than was previously thought because most of what used to present to emergency departments were not actually emergencies).

In spite of these lingering barriers, enough patients are choosing the higher-value options that providers and insurers still have a strong incentive to innovate to improve their value so they can win the market share and profit rewards available to higher-value competitors. And the result is that Americans are being kept healthy more often and are receiving care that is higher quality and more affordable.

That concludes my imagined description of how the American healthcare system could look with the principles from the Healthcare Incentives Framework fully applied. Just as a reminder, it represents merely a guess of how it could end up given the current system. This is by no means the only way to apply the principles of this framework, nor is it my secret idealized version of how it could end up. But I hope it was useful and thought provoking as a case study!

We have come a long way in this series. Throughout it, I worked hard to make the principles of the Healthcare Incentives Framework clear, and I hope the concrete examples have helped solidify those as well as demonstrate their potential for sustainably fixing healthcare systems around the world. If you want a more academic treatment on this framework (at least the part of it that applies specifically to providers), I published that as a medical student.

I intend to help policy makers of all types find ways to apply the principles discussed in this series. Please contact me if you have questions or would like me to help work through potential applications. Contact info is on my About Me and This Blog page. In the meantime, I hope you will follow along as I continue to blog about how to fix our healthcare system!

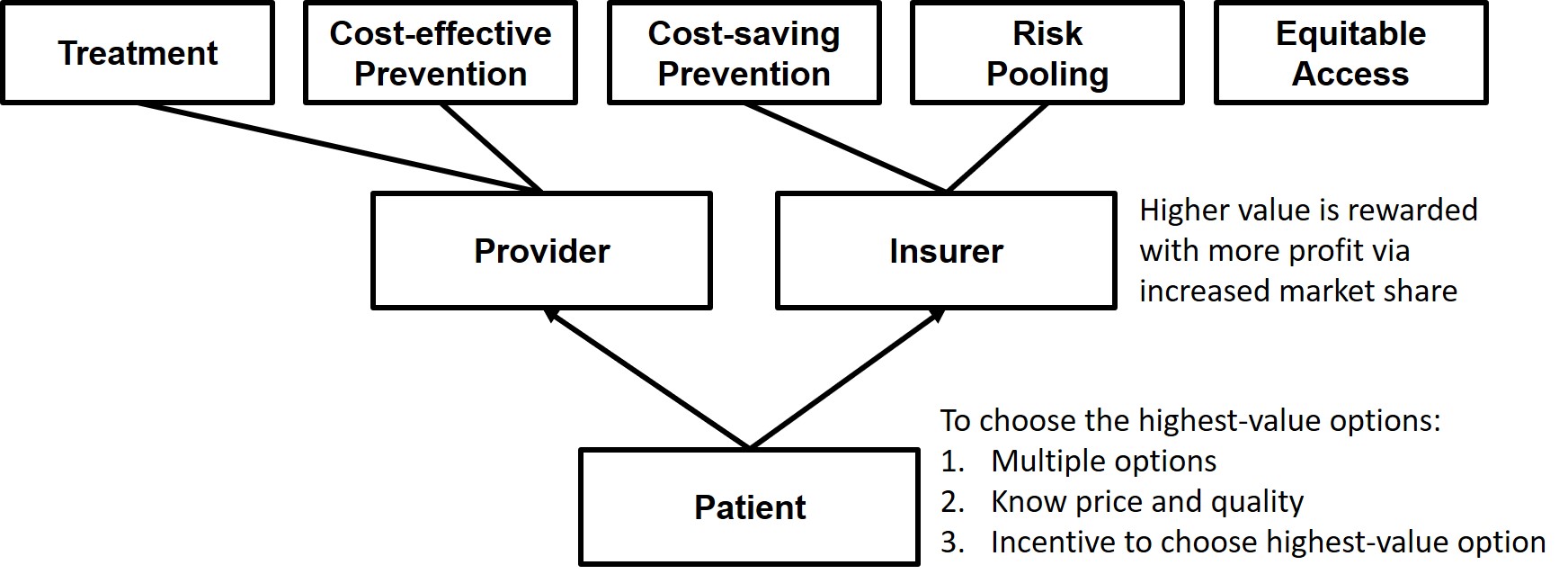

In Parts 1 through 6, I explained the Healthcare Incentives Framework, which is useful for clarifying the necessary ingredients of an optimal healthcare system. Those are the pre-requisite readings to understanding this post, and I will not fully summarize or provide the rationale for them here. But, just as a reminder, Parts 1 through 6 culminated in the goal of getting market share to flow to higher-value providers and insurers, which would be enabled through three critical inputs to decision makers/patients: (1) multiple options, (2) the ability to identify the highest-value option, and (3) incentives to choose the highest-value option. As barriers to those three inputs are minimized, any healthcare system will begin to evolve to deliver higher and higher value. This is the only way to unlock sustained value improvement in healthcare systems.

An important point about this framework is that it is, in a sense, welfare-spectrum neutral, meaning the principles apply to healthcare systems that sit at any point on the welfare spectrum, from libertarian-type systems to fully government-run systems.

Now let’s imagine up some concrete examples of what different types of systems might look like if we built them from scratch using the ingredients from the Healthcare Incentives Framework.

A Libertarian-type System

In this system, there are many private insurers all offering creative and innovative health insurance plans. Their efforts are focused on trying to maximize cost-saving prevention so they can lower their costs and then outprice their competitors. This has led to many ways of keeping people out of hospitals and emergency departments. But since health insurance is an inherently complex product, there are some standardized levels of coverage that have been agreed upon to help people compare those plans apples to apples. This standardization has been implemented in a way that maximally improves comparability with minimal limitation on plan design flexibility. Multiple health insurance comparison shopping websites have arisen, all highlighting those standardized coverage levels, differences between plans, and clear pricing.

An important aspect of these insurance plans is that most of them require the enrollee to pay some part of the price differential between providers; this did not need to be mandated because insurers found that they are able to price premiums more aggressively when they have implemented those cost-sharing characteristics. The plans that do not have this feature are much more expensive, but some people prefer them because they don’t ever need to worry about prices when choosing providers.

There is no requirement for people to buy health insurance, but because there is also no guarantee of care if someone without insurance has a catastrophic medical expense, many people are motivated to buy catastrophic coverage. The rest of their care they buy a la carte out of pocket.

Many of the poor, as well as people with chronic expensive medical conditions, are priced out of the insurance market, but private charities have cropped up that assist with this for most of them.

Looking at the provider side, nonprofits have played a leading role in establishing standards in provider quality metric tracking and reporting. These nonprofits also certify the quality information being reported by providers, so patients are able to compare the quality of different providers apples to apples. The quality metrics being reported and certified are determined by what patients find most relevant in helping them decide between providers for each service they are shopping for. Similar to the health insurance shopping websites, there are provider shopping websites presenting those standardized metrics alongside providers’ advertised prices.

Because providers are assured increased market share when their value goes up relative to competitors, there is a great variety of innovation toward crafting high-value care experiences for patients. Most of the value improvements are in the form of cost-lowering innovations because of the downward pressure on price exerted by the uninsured population and the price-sensitive insured population. Providers have particularly found that shifting the location of care to less expensive settings (including even the patient’s own home) and shifting to relying more on narrowly trained provider types (particularly for treatments that are relatively algorithmic) is very effective at lowering costs. Suppliers of healthcare devices have also found that they are more successful as they focus on developing lower-cost devices, even if that means sacrificing some amount of quality or features. And since government regulations have been kept to a minimum, all these innovations have been allowed to progress and flourish quickly. This occasionally results in unsafe practices and devices cropping up, and individuals have been hurt in the process, but people have felt that the rapidity of innovation that has improved so many lives has been worth that cost. And any practice that proves to be unsafe is exposed quickly in this marketplace.

Providers have also found that, when patients are shopping for a provider, they are looking for a specific well-defined service or bundle of services, such as a year’s worth of chronic disease management, a CT scan, a hip replacement (including all the pre-op workup and the post-op rehab), or a diagnostic evaluation. This has led to standardized bundles of services (also certified by those non-profits), which has made shopping for healthcare services easier and also enhanced the ability to compare the prices from one provider to another.

This system is not perfect. Some people choose not to buy insurance and then have to declare bankruptcy when they have an expensive care episode (or end up not getting care due to inability to pay), and some people want to buy insurance but are frustrated that they cannot afford it, although this number is decreasing each year. Providers face challenges dealing with multiple insurance plans with different reimbursement schemes and coverage rules. And unsafe practices or innovations crop up every so often that harm patients. But, overall, the value delivered by insurers and providers increases rapidly as insurers find new ways to prevent care episodes, and, for the care episodes that cannot be prevented, providers find ways to make care safer, more convenient, and more affordable.

A Single-payer System

With the government running the single insurance company for this system, they have been able to easily implement many of the needed aspects of an optimal healthcare system. They automatically cover all known cost-saving and cost-effective preventive services without copays, which includes population-based preventive services but also focuses more and more on targeting extra services to high-utilizing patients to prevent hospitalizations and ED visits. Their cradle-to-grave time horizon has helped this immensely.

The prices the insurer assigns to services are not firm but are rather considered to be the “maximum allowable reimbursement,” so any provider that wants to charge a lower price will have the freedom to do that. And providers who innovate and find ways to charge less win market share because the insurance plan’s cost-sharing policies require people to pay less out of pocket when selecting a less expensive provider. The insurer has also found that paying a single fee for standardized bundles of services has motivated a great deal of provider innovation and cooperation.

Together, all these reimbursement policies help to prevent as many care episodes as possible and minimize the cost of the episodes that are not preventable.

The insurer’s fee schedule also includes a multiplier to adjust for regional cost variations, and they leverage this to increase reimbursement in underserved areas as well, which has especially helped rural areas maintain enough providers.

As a condition of being accepted as in-network by the insurance plan, providers are required to use an electronic medical record that is able to decode and record to the patient’s secure cloud-based personal health record. Providers are also required to report specific quality metrics. These quality metrics are never used for giving bonuses, but they instead focus on the aspects of quality that patients find most relevant when they’re trying to decide between provider options. The insurer operates a single website that lists all in-network providers along with these risk-adjusted quality metrics and each provider’s prices (displayed as the amount the patient will be expected to pay out of pocket).

Providers appreciate this system for many reasons. They only deal with a single insurer, which minimizes insurance-related overhead expenses and gives them a single set of incentives to respond to. They are completely free to build hospitals and clinics wherever they think they will be most profitable. And they can organize care however they want provided they adhere to the safety and reporting regulations.

Now, having seen the main aspects of this system, let us consider the impact of not adhering to the Healthcare Incentives Framework’s requirement of having multiple insurer options. Recall that the jobs insurers are primarily responsible for are risk pooling and cost-saving prevention. And the reason having multiple options is desirable is because—assuming patients can identify and then choose the highest-value insurance plans—insurers will have a profit motive driving them to innovate to find ways to increase the value they deliver, which especially means finding ways to do more cost-saving prevention that will result in more care episodes being prevented, thus lowering the total cost of care and insurance prices. With a single government-run insurer, that innovation and its attendant benefits will be curtailed. Clearly there are many compensatory benefits, including simplicity, reduced administrative overhead, uniform incentives, and a straightforward way of achieving a society’s goal of universal access to insurance. Depending on the priorities of the country, these benefits may outweigh the costs. It is a question of values. But the decision becomes clearer when the costs and benefits of each option are understood.

A Government-run System

This system, like the single-payer system described above, has a single insurer that is run by the government. But here the government also owns all the healthcare facilities and employs all the healthcare providers.

On the insurance side, reimbursement policies are familiar, with “maximum allowable reimbursements,” bundled pricing, differential cost-sharing for patients, and a website reporting the quality metrics and prices (out-of-pocket costs) of providers. The insurer also has a robust department working on preventing care episodes by finding innovative ways to keep people healthy.

But what about the provider side? Initially it may seem that patients only have a single healthcare provider option, but just because a single entity owns all the hospitals and clinics does not mean they are all the same. In this system, the government determines where healthcare facilities will be built and what services they will provide, but it allows great freedom in their operation. At every facility, providers are able to organize care however they like, and they are also free to charge any price as long as it is at or below the maximum allowable reimbursement for each service. They have great motivation to put in the effort required to find ways to lower costs (thereby enabling them to charge lower prices) and improve quality because they receive bonuses that are calculated based on the amount of money they saved the system (the number of patients treated multiplied by how much less than the maximum allowable reimbursement each of those patients was charged).

Because the insurer and providers are all operating under one roof, the billing in this system is particularly simple. Some specific requirements are in place for the purpose of accumulating data that will help track for problems in the healthcare system, but there are no complex billing codes or arcane documentation requirements. When providers document a patient encounter, they do so for the purpose of communicating to other providers what they thought and did.

Government healthcare expenditures in this system are sustainable mostly because providers are actively innovating to improve value—much of which results in them being able to lower prices so they can earn bonuses.

Overall, this system has been organized in a way that, despite the government ownership of providers, maintains the ability to reward value with market share, which drives value improvement. The insurance side also innovates to prevent care episodes by leveraging its cradle-to-grave time horizons and connections with other non-healthcare public health sectors.

There are barriers to provider innovation compared to other systems. Providers face the upside of potential bonuses for doing well, but there is not necessarily much downside risk in providers who are mediocre or worse and still getting paid their stable salary. In any other market, the risk of being forced out of business due to lost market share drives competitors to innovate to improve their value so they can become profitable, but in this system the worst-case scenario is that the government closes their clinic and relocates those providers elsewhere. Additionally, many innovations require new types of facilities or caregivers, or they require cooperation between multiple types of providers, which can be difficult when providers have limited control over facility design, placement, and reimbursement contracts.

The effects of these innovation barriers are difficult to quantify, but they need to be balanced with the benefits of a reduced documentation burden, a simpler billing system, and a more reliable dispersion of healthcare services across the country.

Conclusion

Policy makers overseeing any type of system need to understand their system’s current barriers to the three critical inputs: multiple options, ability to identify the highest-value option, and incentive to choose the highest-value option. (Many of the most common barriers to those three inputs are outlined in Part 6.) They need to understand that those barriers are the primary inhibitors of their healthcare system evolving to deliver increasingly higher value for patients over time. And as they enact policies that eliminate those barriers, they will see a predictable chain reaction of more patients choosing higher-value insurance plans and providers, those higher-value competitors earning more profit, and parties in the healthcare system beginning to innovate to deliver higher value, all of which will result in the healthcare system transformation that is sorely needed the world over. Policy makers who understand this Healthcare Incentives Framework are also empowered to propose and support policies that expand access in ways that do not create new barriers to those three critical inputs.

As healthcare reforms begin to take this focused direction, the innovations and value improvements will be exciting to watch!

In Part 8, I will conclude this series by imagining how the U.S. healthcare system might look with the Healthcare Incentives Framework fully implemented.

In Part 5, we talked about the three requirements for getting market share to flow to the highest-value options, which is necessary if we want higher-value parties (insurers and providers) to be rewarded with profit. The context for why this is the crucial feature of our optimal from-scratch healthcare system is discussed in parts 1, 2, 3, and 4.

As a reminder, those three requirements were for patients to have (1) multiple options, (2) the ability to identify the highest-value option, and (3) incentives to choose the highest-value option. Let’s look at examples of the common barriers to each of them so we will know what to avoid when we build our optimal healthcare system.

Multiple Options

Our goal: Avoid any policies that directly or indirectly limit the number of competitors in a market.

For providers, this means allowing them to build hospitals and clinics whenever and wherever they want. They will not do this with reckless abandon because they will know that, if they choose to build in a new region and end up delivering lower value than the incumbents, they will not get many patients and their new endeavor will not be profitable.

For insurers, this means avoiding regulations that make it difficult for them to enter new markets. Nationally standardized regulations will simplify the process of selling insurance in multiple markets, but this does nothing to ease insurers’ greatest challenge of entering new markets, which is the challenge of negotiating prices with providers in that region. But having many provider options in a region should help with this.

And as for things that affect both providers and insurers, we will need good antitrust laws to prevent too much consolidation. And we will need to avoid policies that limit the freedom of them to vary their price and quality so that they can offer unique value propositions (otherwise we end up with many options that all are effectively the same, which defeats the purpose).

Identifying the Highest-value Option

The barriers to this are different for providers and insurers.

On the insurer side, the most difficult aspect of identifying the highest-value option is being able to predict which mixture of premium, copay, deductible, coinsurance, etc. will cover what you need in the cheapest way possible, as well as identifying/predicting which services will be needed and whether they are covered in the benefits. Having some standardization can make this much simpler (but still challenging), such as what healthcare.gov does with multiple standardized quality tiers of insurance plans and grouping all those options together to be compared apples to apples.

On the provider side, one of the first challenges is getting people to recognize that they have multiple options that are of very different value. In almost every other industry, people are great value shoppers, but they have been conditioned historically not to even think about it when choosing healthcare providers, which is probably a consequence of the chronic unawareness of the huge variations in the quality of providers as well as the third-party payer system that so often causes people to pay the same no matter which provider they choose. This is one reason why healthcare provider quality reporting websites are so infrequently used even when they are available.

The other issues with identifying the highest-value providers can be divided into barriers to knowing price beforehand and barriers to knowing quality.

Barriers to knowing price beforehand: The biggest one is uncertainty about what services will be needed—for example, most people do not present to the emergency department with a diagnosis already, nor can they predict what additional complications might arise during a hospitalization. But for specific, well-defined episodes of care, such as an elective surgery, there are great ways to make prices knowable beforehand (look up bundled pricing for an example).

Barriers to knowing quality: People do not know where to find quality information even if they do go looking for it. And if they find it, most of what they find are quality metrics geared specifically toward comparing providers for the purpose of allocating bonuses rather than quality metrics that actually provide metrics that are relevant to helping a patient choose between providers. For example, a hospital’s overall mortality rate or readmission rate has little bearing on the quality of care a patient will receive for something like a straightforward elective gallbladder removal. Standardized, easy-to-understand, appropriately risk-adjusted, patient decision-oriented quality data are needed.

And the last thing to mention in this section are the barriers to identifying the highest-value option that will not likely be overcome. For example, medical emergencies don’t allow time to make a thoughtful decision about which hospital to go to. And low health literacy is a barrier for many people. And there are many important aspects of care that cannot easily be measured, such as a primary care doctor’s ability to diagnose the cause of ambiguous symptoms. Does the presence of these more insurmountable barriers mean that no health system will ever be able to get market share to flow to the higher-value options? No—even if many decisions about which provider to go to are not particularly logical or value-focused, as more people start choosing providers based on price and quality information, higher-value providers will begin to win more market share and the desired incentive scheme that motivates value-maximizing behaviors will arise.

Incentives to Choose the Highest-value Option

Even when people (1) have multiple insurer and provider options and (2) are able to identify the highest-value options, there are still barriers to them choosing the highest-value options.

The first barrier is when anyone but the patient is acting as the decision maker. These alternative decision makers typically have a financial stake in the decision and want to choose the cheapest option without regard for quality. For example, insurers that offer very narrow networks act almost like a first-cut decision maker to narrow patients’ possible provider choices down to only providers that are willing to accept the lowest prices. Patients/patient advocates should be the decision makers because only they will adequately weigh the quality aspects that are most important to and impactful on them.

But even when the patient is the decision maker, they will ignore prices if they are required to pay the same amount regardless of the provider or insurer they choose. This is usually not an issue with insurance plan selection, but it is a major issue with provider selection. For example, flat copays require the same payment from the patient regardless of the full price of the providers. High-deductible plans solve this problem for any service below the deductible, but, once that deductible is surpassed, they have the same problem. Ideas such as reference pricing, multi-tier provider networks, or even paying patients for choosing lower-cost providers can help with this.

Summary

If the above discussed barriers to the three requirements for getting market share to flow to the highest-value options are minimized, the healthcare system will naturally and continuously evolve toward higher value because it will motivate providers and insurers to perform their jobs in value-maximizing ways. Government interventions may still be considered for areas where natural incentives will not motivate those parties to do all the jobs we want them to do (particularly in the area of equitable access), but the “healthcare market” will start functioning to benefit patients and what they value.

This concludes the big-picture explanation of this Healthcare Incentives Framework. In other words, we have now discussed all the ingredients that need to go into an optimal from-scratch healthcare system. In Part 7, we will solidify the implications of this framework by imagining up a few examples of different types of healthcare systems with the Healthcare Incentives Framework implemented to show how all those ingredients can come together.

We established in prior parts of this series that, in this Healthcare Incentives Framework, there are specific identifiable jobs we want a healthcare system to do for us, and that there are parties that have incentives to perform those jobs for us. The focus then turned to how to get those parties to perform those jobs in ways that maximize value, which we saw is achieved by rewarding them with more profit when they perform their jobs in higher-value ways. And in Part 4, we saw that the only effective way to do that is by getting market share to flow to the higher-value options. In this post, we examine what needs to happen for people to choose those higher-value options.

There are three requirements that all must be in place at the same time to enable someone to choose the highest-value option:

Requirement 1: Multiple options. This one seems straightforward–no market share can flow anywhere if there is only one option available. But there is another, less obvious aspect of this. Parties also need the freedom to vary their price and quality in ways that create unique value propositions, otherwise they will all look pretty similar, so the effective options people have would be severely limited, even if the total number of options is not. For example, if there is a price floor created by some administrative pricing mechanism, it will prevent any innovation that lowers quality a little bit but significantly lowers price. Why? Because those parties contemplating that kind of innovation will know that, without the ability to offer prices significantly lower than their competitors, they will be unable to win the market share necessary to make their innovation profitable.

Requirement 2: Ability to identify the highest-value option. Remember that value is determined by two things: quality and price. People choosing from among multiple providers or insurers need to be able to compare, apples to apples, the quality and price of all their options before they select one. But having apples-to-apples comparable price and quality information is not enough. The quality information would have to be simple enough to be easily understood and also relevant to the specific dimensions of quality people actually care about. And price information would need to reflect the expected total price of the product or service, otherwise it’s mostly useless. Both quality and price can be challenging in healthcare, which creates barriers to people being able to identify the highest-value option, but those barriers will be discussed in part 6 of this series.

Requirement 3: Incentive to choose the highest-value option. Even if people have multiple options and are able to easily tell which is the highest-value option, they will not choose that highest-value option without the right incentives. This applies to both their insurance plan selection and their care providers selection. Consider this example about choosing the highest-value care provider: suppose a patient has the choice to have a procedure at a nearby world-renowned hospital (95% success rate, $80,000) or the local community hospital (92% success rate, $40,000). Further suppose that this patient will pay $10,000 out of pocket (their annual out-of-pocket max) regardless of which hospital they choose. Which will they choose? An additional 3% chance of success for an extra $40,000 seems steep, but since they’re not paying the difference, most people would go for the world-renowned hospital regardless of the difference. Extracting the principle from this example, people need to pay more when they choose a higher-priced provider (or less when they choose a lower-priced provider); this doesn’t necessarily mean they always need to pay the complete difference between the two, but they at least need to pay some of that difference. Same goes for the quality aspect of value. If someone other than the patient (say, the insurance company) is choosing where the patient will receive care, they generally care a lot more about the price than about the quality differences between the options since they aren’t the one who bears the consequences of going to a lower-quality option. So, in summary, regardless of whether the discussion is about choosing providers or choosing insurance plans, the individual making purchase decisions needs to bear the price and quality consequences of the decision.

By now it should be clear that if any of these three criteria are not fulfilled, market share will not flow to the highest-value options, and the whole incentive scheme we are creating falls apart.

There are, you may have figured, many many barriers to these things working in current healthcare systems, some of which would be present even in our optimal healthcare system we are building. But that’s the topic of Part 6.

Have you had the experience where you need a medication, and the brand name actually is cheaper for you because your doctor gives you a coupon for it? It’s great for you, but it’s bad for the healthcare system, and here’s why.

I have written before about the principle that is relevant to this, but it bears repeating: The party making a purchase decision must be the one who also bears the price differential between those options.

To understand why, let’s pretend you have a medium risk of heart attack or stroke in the next 10 years, so your doctor recommends you start a moderate-intensity statin medication. They’re all pretty close to equal in terms of efficacy and side effects, so the best money-saving decision would be to choose the cheapest one, right? Well, if your doctor says, “I’m happy to prescribe any of these for you. Which would you like?” You are the party who now gets to make a purchase decision. So you look at the monthly prices below (these are real prices):

But then your doctor hands you a pitavastatin $100 off coupon some drug rep from Kowa Pharmaceuticals (the manufacturer) dropped off. You, a rational person, opt for that one since it’s now the cheapest (free)!

Now the monthly cost to the healthcare system for you to be on a statin totals $0.00 (your copay) + $101.36 (what your insurer has to cover) = $101.36. That’s about 20 times more expensive than it should have been!

What just happened here? The party making the purchase decision (you) did not bear the price differential between the options. Your insurer originally set it up so that you would pay more if you chose a more expensive statin, but the coupon interfered with that.

This same situation plays out over and over every day in our healthcare system with medications and with every other health service. It’s why I keep saying that we need to make the party who makes the purchase decision the same party who bears at least some part of the price differential between the options, which leads to a value-sensitive decision. Reference pricing does it, high-deductible insurance plans do it (for services below the deductible, at least), multi-tier prescription programs do it (when they’re not being subverted by manufacturer coupons). But these, collectively, are not influencing nearly enough of the purchase decisions being made in our healthcare system! And we waste money. Even worse, the higher value options are not rewarded with market share, the lower-value options are allowed to persist as is, and the overall value delivered by our healthcare system remains much lower than it could be.

So that’s why medication coupons–and any other thing that interferes with purchasers bearing the price differential between options–are bad.

First off, I apologize for the long delay between blog posts. I’m still here, and I still am obsessed with health policy. I’ve been working on a publication that outlines some of what I’ve figured out lately, and I’d rather people first see it in a publication by me rather than by someone else who came across it on my random blog and ran with it.

Anyway, let’s talk about why insurers are starting to do things differently lately. They’ve started doing pilot projects to see if investing in primary care will save them money by preventing unnecessary tests and services (they predict it will in a big way). They’ve also started investing more in IT to keep track of patients’ health information, again hoping they can use it to find ways to prevent patients from needing preventable tests and services.

Of course this makes sense. If they, as a business, can invest $500,000 in primary care and then save $600,000 by preventing a whole bunch of things down the road that they otherwise would have had to pay for, it’s a great investment! But why haven’t they started trying out these investments in cost-saving prevention until now? Remember that a business is always trying to use the money they’re making and invest it in projects that improve their financial performance. But there are a lot more options of projects to invest in than they have the money to invest. So they are trying to find the projects that seem to offer the greatest reward for the lowest risk. This would lead us to assume that these kinds of projects haven’t had a great reward-risk ratio until now.

I haven’t figured out a great way to organize my thoughts about this, so here they are in a random order. (FYI, one of the items in the list below is going to change, and it explains why insurers are changing their ways, so you better figure out which.)

If an insurer wants to invest in prevention, but then the patient switches insurance before the insurer gets to reap the savings, that was basically wasted money. Yeah the patient is healthier as a result, so that’s a small consolation prize, but the analyst who forgot to compare the expected payback period with the average length a patients stay on their insurance will probably still be fired.

Trying to pay a primary care physician to do better at keeping patients healthy isn’t an across-the-board money saver. Actually, it probably only saves money for a small portion of patients. But the thing that makes it worth it is that those patients are probably the highest-cost patients, so a ton of money still stands to be saved.

Paying a physician more to establish a medical home or hire a care manager or something like that probably involves the insurer paying the whole cost for the physician to do that, otherwise they won’t. And since the physician has the care manager, chances are he/she will use that care manager for all his/her patients who need the service, including patients that are covered by other insurers. So the insurer is now stuck paying for a competitor’s patients to get healthier, saving the competitor money even though the competitor didn’t invest a thing.

An insurer won’t be very popular if they add services to only a select group of patients on the exact same coverage plan. Other people will say that’s unfair and demand to receive the same service. This would be annoying, and they’d have to find a way around it so they don’t end up spending all this prevention money on people who won’t end up saving them much in return.

People, when buying insurance plans, aren’t really able to compare the coverage offered by different plans. There are so many complexities, all they can really do is look at the price and look at some of the basic coverage provisions, but that’s it. There may be all sorts of limitations that they don’t even know about. Because of this, insurers can get away with offering a high-priced plan with not great coverage and still (through great marketing) convince a lot of people to buy it, so where is the reward in finding ways to lower price by doing cost-saving prevention when you can just add a few exclusions to save money instead and nobody will ever notice when they’re choosing their insurance plan?

I hope you figured out that the last one is changing. With new tools coming out that help people more easily compare the quality of coverage offered by different health plans, including insurance exchanges’ standardized levels of coverage, people will be able to spot the insurance plan with equivalent coverage but a way lower price. And when that happens, people will flock to that insurance plan. This is a significantly larger incentive to try out risky investments in cost-saving prevention, which also means it’s quite a risk not to try anything out for fear that you’ll lose all your customers. Finally, cost-saving prevention projects that actually decrease overall health spending and keep patients healthier will top every analyst’s list!

And in case you’re wondering what role increasing health costs have played in this whole thing, the answer is . . . probably nothing. Health costs have always risen, and insurers have always raised premiums to maintain pretty constant profit margins. Sometimes spending increases slower and they make a bundle, sometimes costs rise faster than predicted and they increase premiums even more the next year. But none of this changes the risk-reward evaluation done by analysts to decide if they should finally start to invest in cost-saving measures, although it might in an indirect way because people are clamoring louder (as costs rise) to get cheaper health insurance, but unless those people were finally able to compare the value of different plans, all their clamoring wouldn’t have much of an effect on insurers’ investment strategies.

Most reform proposals will make care less expensive for patients (due to more integrated care plans, a better focus on preventive care, fewer complications, etc.)

Providers are the ones charged with making these delivery changes

Patients saving money = providers getting paid less

Why would providers make the changes only to lose money? They somehow need to financially benefit from their efforts and improvements

Are there solutions to this? Of course! Here are my favorite two:

First, integrated delivery. If the organization charged with making changes to how care is delivered is the same that will benefit financially, it works. An example might help. I live in Utah, where Intermountain Health Care (IHC) dominates. IHC is really good about doing research and finding ways to improve quality. So let’s pretend they do a lot of heart valve replacements, and that they’re usually paid $20,000. But, if they have a complication, they have to do all sorts of extra work, and they end up getting paid $30,000. (I’m making the numbers up, but I’m not lying about the fact that providers often get paid more for procedures when there were complications.) So, IHC finds that they can tilt the bed at a 20-degree angle and that magically reduces complications by 25%. But that means they’re getting paid $10,000 less every time they avoid that complication! The patient whose complication was averted with the tilting of the bed maybe ends up paying $2,000 less in co-pays than he would have, and the insurance company saves the other $8,000.

Poor IHC, right? They spent thousands of dollars on the research that produced the bed-tilting idea, and now the patients’ and insurance companies’ wallets are benefitting. Except, IHC has a secret. The insurance that patient was on is Select Health, which is IHC-owned! So, really, IHC just saved its patient $2,000 and saved itself $8,000. Not bad! This scenario, when the provider and insurer are the same entity, is called “integrated delivery,” and it creates excellent incentives to improve quality. The only time this breaks down is when IHC averts all sorts of complications for patients on different insurance companies. [Update: There are downsides to integrated delivery organizations, including ACOs, that relate to their limiting of the options available to patients and, thus, interfere with value-sensitive decisions. I won’t explain it here, but I’ve learned more since writing this post.]

This brings me to the second solution, which can sometimes work when it’s not an integrated delivery situation. So when IHC goes to renegotiate their contract with, say, Altius, they will have their reduced-complication-rates data in hand, and they will say, “Hey, we have 25% fewer complications than before, so your average cost will go down from $22,500 to $21,000. But we want some of those savings since you didn’t do anything to warrant saving all that money, so we’ll raise your rates a little bit to make your average cost $22,000, which is still lower than it was before, and we’ll be getting some compensation for all this hard quality-improvement work we’ve been doing.” I guess this solution could be called “splitting the savings.” [Update: Since writing this, an amazing idea called “shared savings” became popular. It’s exactly what I describe above. But it has a pithier name.]

The providers will still be losing some of the savings to the patients and external insurance companies, but at least they’re improving quality and their reputation!