Since we’ve just been through Black Friday and Cyber Monday (Cyber Week now?), I thought this would be a fitting topic.

Let me start with the premise of why shopping for healthcare services is important: The only way to sustainably improve the value delivered by healthcare systems is to get people to start choosing higher-value providers and insurance plans. But how many health services are actually shoppable? This is not something I’ve written about before, and it’s because I am not sure of the answer. But here are some beginning thoughts on the topic.

First, I believe all insurance should be shoppable. No, people will not have perfect information about all the quality aspects of the insurance plans, nor will they be able to perfectly predict which cost-sharing arrangements will be cheapest for them, nor are all people mentally equipped to sift through this complex information, but major quality and price differences between different insurance plans should be clear for most people if the shopping experience is well designed.

Health services are another matter. And any effort to quantify the shoppability of health services should be broken down into two analyses:

- What percent of services are shoppable?

- What percent of spending is attributable to those shoppable services?

The second question is arguably more important if you are concerned with the fiscal stability of countries dealing with runaway healthcare spending. But you can only answer the second question after you answer the first question.

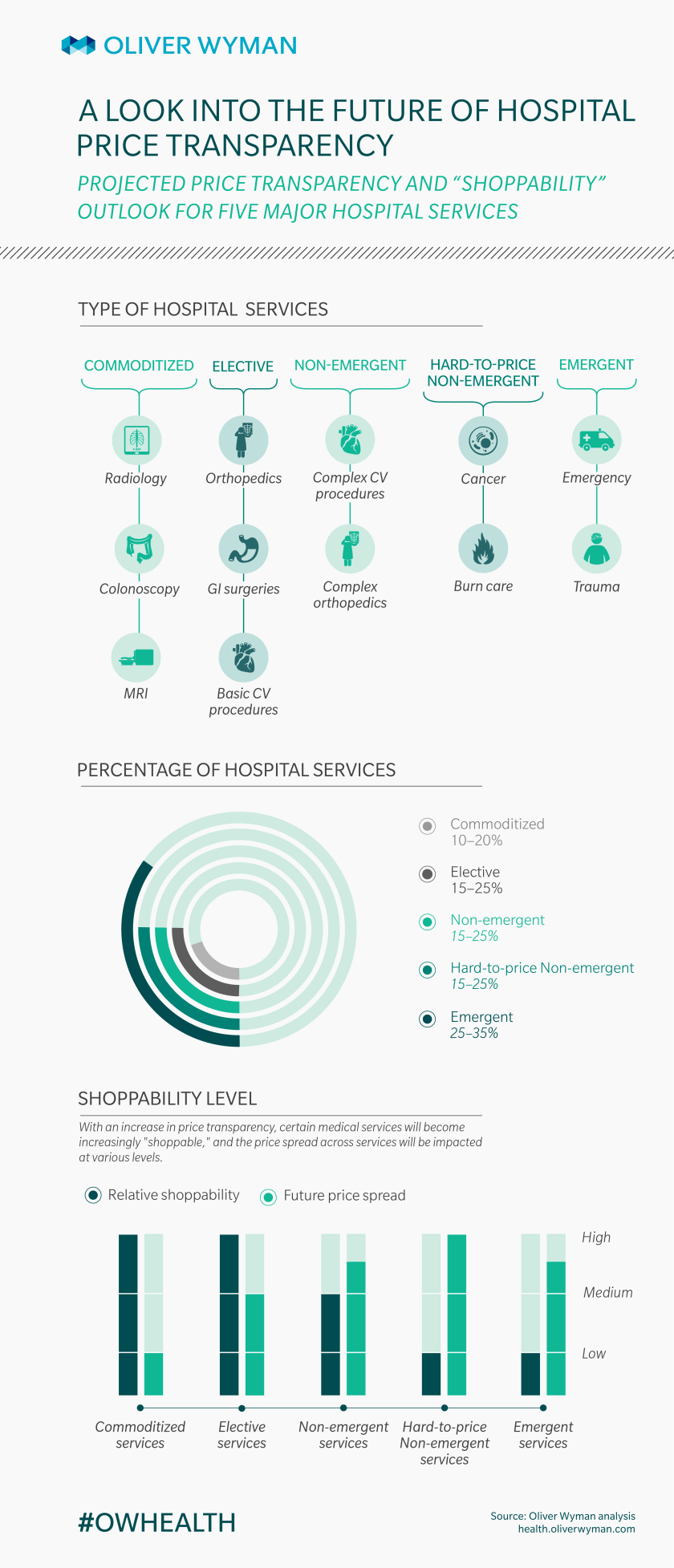

Since I like exhaustive, mutually exclusive categorizations, I enjoyed this breakdown of the first question:

I’ll point out that they only considered hospital services. But one thing I like is how they considered how commoditized something is (how easy it is to shop for that service because quality is pretty standardized) and accounted for that when predicting how much prices will drop.

If I were to create my own categorization scheme, I would start with an emergent category. Not very many services are actually emergent requiring an ambulance ride straight to the nearest hospital that has capabilities to deal with the issue at hand. A quick thought to my residency days working in ICUs and EDs brings to mind the major things like acute coronary events, strokes, major trauma, sepsis, and acute respiratory failure.

What percent of spending is in this emergency category? It’s tough to calculate because emergency department charges alone don’t account for subsequent hospital care for those medical problems. But this report by the Health Care Cost Institute at least gives a few numbers that could help us ballpark it, and I’d put the total spending on emergencies at around 5-20% of total healthcare spending. Maybe there are better analyses out there on this very thing, but I haven’t seen them.

Once we’ve ruled out the emergent events, we’re left with the other category: everything else. These things could all theoretically be shoppable, but there are some with potentially insurmountable barriers. For example, some services have no easy-to-identify quality metrics (such as ambiguous symptoms requiring a diagnosis–how do you choose the right provider to diagnose that?). And other times, patients are not able to easily predict which services will be needed (such as when an elderly patient with multiple comorbidities goes to the emergency department with shortness of breath).

I could subdivide nonemergent health services into two categories: diagnostic services and treatment services. Per the examples in the prior paragraph, diagnostic services are harder to shop for. Treatment services are typically easier to shop for (like when you know you need a specific surgery). But there are times when the treatment of a condition is not easily separated from the diagnostic efforts. For example, if an orthopedic surgeon diagnoses you with knee osteoarthritis requiring a knee replacement, you typically won’t shop around for the highest-value knee surgeon–you’ll just get the surgery by the doctor who made the diagnosis (not that second opinions are impossible). Or, if you went to a specific hospital’s emergency department and were found to have a heart failure exacerbation requiring hospital admission, you don’t hop on your smartphone and start comparing which hospital can best treat that–you just get admitted to the hospital you’re already in.

So I guess I’m saying that diagnostic efforts are hard to shop for, and treatment efforts that are naturally connected to those diagnostic efforts are also hard to shop for.

How about some numbers? This analysis by the National Institute for Health Care Reform estimates that at least 70% of inpatient spending is shoppable, and 90% of outpatient services are shoppable. But then later they wrote that, when accounting for all potentially shoppable services in our healthcare system, those services account for only about 1/3 of total healthcare spending.

Clearly there is more to learn and discuss about this topic.

A couple parting thoughts: Keep in mind that, regardless of what percent of services or spending is not shoppable, it doesn’t mean we should give up on enabling patients to shop for as much as they are capable of. Getting them to choose higher-value options is still the only long-term solution to improving the value delivered by healthcare systems, as explained in my Healthcare Incentives Framework. And there will likely be a positive externality effect on non-shoppable services when providers up their game on shoppable services.