In Part 26, I teased that President was about to make some changes to the laws to bring about a uniform currency. Let’s see what he does!

As a preface to this part, you should know that this was the most difficult transition in the entire evolution of money for me to figure out. The information on this specific aspect of the history of money is much less readily available. But I’ll do my best to explain how this has happened in the real world many times before, and I’ll attempt to do it in a logical order without skipping any steps.

With the goal of making First Bank Goldnotes the standard common medium of exchange countrywide, President creates two new laws:

First, there will be a tax on the lending of non-First Bank Goldnotes. So, from that point on, any time another bank loans out their own Goldnotes and earns interest on them, they have to pay, say, 5% of the total loan value to the government in the form of taxes. That’s pretty high, especially considering that most loans are probably earning less than that.

Second, banks are allowed to switch out their own Goldnotes for First Bank Goldnotes by sending all of their gold coins (and other acceptable assets) to First Bank. Non-cash assets that are being used as reserves for lending, such as the cars that Storybook Bank found itself owning back in Part 22, may or may not be accepted by First Bank, and the bank that owns those non-cash assets may just have to retire those assets from their role as reserves once the loans made based upon those assets have been repaid.

The first law makes it no longer profitable to lend out their own Goldnotes. It became much cheaper instead for banks to transact using First Bank Goldnotes, which gives them a big incentive to take advantage of the opportunity offered in the second law by switching over to First Bank Goldnotes.

Let’s see how this switch would occur with Astro Bank:

First, Astro Bank has to pack up its entire store of specie (gold) and cart it to First Bank. And when it delivers all of its specie to First Bank, in return it will be credited in its First Bank account with an equal amount of “reserve credits.” This dictates how many First Bank Goldnotes Astro Bank is allowed to lend out. For example, if the reserve ratio is 0.2 (money multiplier of 5) and Astro Bank just deposited 4,000 gold coins into First Bank, it will receive 4,000 reserve credits, and each reserve credit allows Astro Bank to lend out 5 First Bank Goldnotes. The details of this will be discussed further in Part 28.

Second, First Bank announces that all Astro Bank Goldnotes are now retired, and there will be an exchange period to allow any holders of Astro Bank Goldnotes to present them to First Bank and, in exchange, they will receive First Bank Goldnotes. For simplicity, let’s assume they just trade them 1:1 straight across. Any existing contracts denominated in Astro Bank Goldnotes will automatically be updated to be denominated in First Bank Goldnotes instead. Then, after that exchange period ends, any Astro Bank Goldnotes that haven’t been traded in will be officially worthless.

So if Astro Bank owned loans that were worth 20,000 Astro Bank Goldnotes, they now own loans that are worth 20,000 First Bank Goldnotes. And just like way earlier in this series (Part 18), whenever Astro Bank receives a loan payment, the interest portion of that payment will go into their Revenue stack of First Bank Goldnotes in their vault and the principal portion will go into their Money to Lend section. Once there are enough First Bank Goldnotes in the Money to Lend section, they can give a new loan. Thus is the ever-rotating cycle of the majority of Goldnotes.

This process turns out to be an offer the banks can’t refuse, and they all agree to it. From then on, they get to avoid the tax on lending non-First Bank Goldnotes, and they don’t even have to worry about finding the storage space for big piles of gold coins in their vaults anymore!

Pay attention to what just happened here. The government (through its bank) essentially seized all of the gold from all of the banks. But it did it through shaping bank incentives just right, no force required. And everyone, including the banks, are pleased with the outcome because Avaria now has a conveniently uniform monetary system.

And that is how Avaria shifted from a decentralized fractional reserve currency to a centralized fractional reserve currency. There are other ways this has been done, including simply by making the printing of receipt money illegal for non-government-approved banks, or by requiring a government license to print receipt money and then not granting any new licenses and letting the old ones lapse over time.

From now on, any time someone wants to exchange a Goldnote for a gold coin, they have to go to a First Bank branch to do so. And just like Peppercorn Bank discovered way back when it invented fractional reserve banking, a low enough percentage of people actually do that that there are always enough gold coins in the vault.

Incidentally, which bank’s “account” would the gold coins come from when someone comes to First Bank with a First Bank Goldnote requesting to trade it for a gold coin?

None. Those gold coins have been anonymized in First Bank’s vaults, so as long as there aren’t too many First Bank Goldnotes in circulation, they will always have enough gold.

But having enough gold in the vaults is becoming less and less relevant of a concern anyway because people are trading out First Bank Goldnotes for gold coins less and less often as they, with time, get used to transacting exclusively in First Bank Goldnotes and come to trust that they are a reliable form of money.

What does President do once all of the other banks’ Goldnotes are completely phased out? He creates a couple more laws to protect the ground he has won.

First, to forever prevent regression back to a multi-currency society, he declares that First Bank now has a permanent monopoly on issuing bank notes.

Second, to reinforce First Bank Goldnotes as the only form of acceptable money in the country (in the unlikely event of a banking fiasco that harms their reputation and tempts citizens to start using something else–such as another country’s currency–as their common medium of exchange), he passes a legal tender law (explained in Part 24) that requires acceptance of First Bank Goldnotes for all debts, public and private.

And to commemorate this change, all of First Bank’s subsequent Goldnotes will be printed with a new pithy name: First Bank Note.

*Moment of silence for the end of Goldnotes*

And on these new First Bank Notes will be the legal tender inscription: “This note is legal tender for all debts, public and private.” Each First Bank Note will still be exchangeable for one gold coin, which can be redeemed at any First Bank branch, so the country’s new official receipt money will still have an anchor to gold to keep its value from drifting arbitrarily.

Oh, one more thing. For simplicity, up to this point I’ve ignored fractions of gold coins, and I’ll continue to do so; but surely this society can have half coins, quarter coins, etc., and it can use any form of receipt money (either with paper or with “token coins,” which are cheap metal coins with their official monetary value stamped on them) to represent those smaller denominations. I just think talking about those smaller denominations doesn’t help the overall explanation and risks adding confusion.

Anyway, in summary, we have finally achieved a centralized (uniform) currency! It’s starting to seem like modern money, isn’t it? Believe it or not, First Bank Notes are still different than modern money in huge ways.

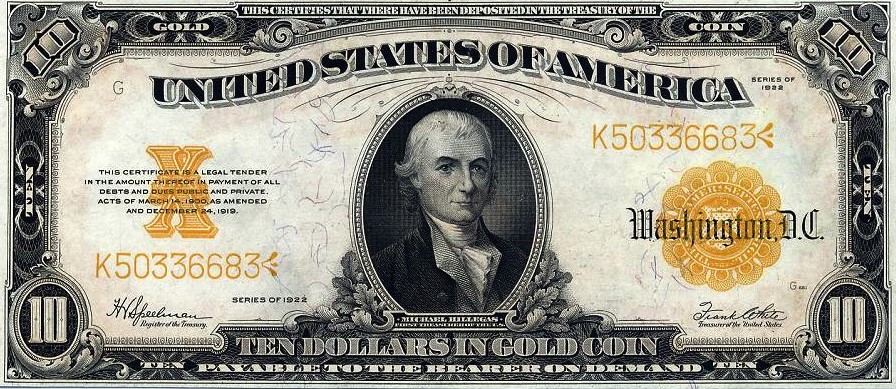

As a little hint about where this series is headed, check out a comparison of two American bills (which, interestingly, are now known as Federal Reserve Notes, which you will see printed on any bill today).

The United States transitioned to a centralized currency in 1913 after the passage of the Federal Reserve Act. Check out this 1922 ten-dollar bill with the following text printed on it: “This certifies that there have been deposited in the treasury of the United States of America ten dollars in gold coin, payable to the bearer on demand.” (Remember that the term “dollar” originally just specified a certain weight in gold.) It also has the legal tender inscription on it.

Now compare that to a more modern dollar bill. This one also has the legal tender inscription (rewritten to be more concise), but notice the change in text: “Federal Reserve Note, The United States of America, one dollar.”

There’s no mention of gold, nor any mention of it being exchangeable for anything else. Interesting, right? . . .

In Part 28, we will process more of the implications of this change before we finish with the last few major money transitions.